The Cost of Living Adjustment (COLA) is an essential economic tool that helps maintain the purchasing power of individuals as prices rise. Adjusting income to match the increasing costs of goods and services ensures people can afford their basic needs over time.

This adjustment is crucial for retirees, disabled individuals, veterans receiving benefits, and others who rely on fixed incomes. Without COLA, their standard of living would deteriorate as prices go up, making it harder to cover daily expenses.

Let’s dive deeper into the concept of cost of living adjustment, the factors that influence it, understand how it is calculated, and see its impact on businesses.

What is the Cost of Living Adjustment (COLA)?

Cost of living adjustment is a change in one’s monthly retirement benefit to account for increasing prices or inflation. It helps maintain purchasing power as prices rise over time. It ensures that the value of retirement benefits remains stable despite economic changes.

In other words, COLAs aim to preserve your ability to buy the same goods and services, regardless of how long you live or how quickly prices increase.

Why is COLA Important?

COLA helps protect people from inflation, empowers them to maintain their standard of living, and allows them to adapt to changing economic conditions.

Let’s understand the importance of cost of living adjustment in detail.

1. Inflation Protection

COLA helps guard against the erosion of purchasing power caused by inflation. It ensures that the value of income doesn’t diminish over time, allowing recipients to afford the same goods and services year after year. This protection is essential for accurate long-term financial planning, especially for retirees and others on fixed incomes.

2. Standard of Living

COLA allows recipients to maintain their quality of life as prices for goods and services increase. These adjustments are necessary for individuals to have to cut back on essentials or luxuries they once enjoyed. By keeping pace with rising costs, cost of living adjustment helps people sustain their lifestyle throughout retirement or while on a fixed income.

3. Financial Stability

COLA provides security for those on fixed incomes, helping to prevent financial hardship. It offers a buffer against rising prices for necessities such as food, housing, and healthcare. This stability enables more informed decision-making about long-term economic health and retirement savings strategies.

4. Economic Adjustment

Cost of living adjustment allows incomes to adapt to changing economic conditions over time. This flexibility helps individuals weather economic fluctuations and maintain their financial footing. It’s particularly crucial for those relying on fixed-income sources like pensions or Social Security.

For example, consider the recent Social Security benefits adjustment:

- In 2023, an individual receiving $20,000 in benefits saw an 8.7% COLA, increasing their benefits to $21,740.

- For 2024, with a 3.2% COLA, the same benefits would total $22,435.68.

How is COLA determined?

The Social Security Administration (SSA) determines the annual Cost of Living Adjustment. Here’s an overview of the process:

1. CPI-W Measurement

The SSA uses the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). This index, maintained by the Bureau of Labor Statistics, tracks average price changes for goods and services.

2. Comparison Period

The SSA compares the average CPI-W for the current year’s third quarter to the same quarter of the previous year.

3. Percentage Calculation

If the CPI-W increases, the SSA calculates the percentage difference. This percentage becomes the COLA for the following year.

4. Annual Announcement

In October, the SSA announced the cost of living adjustment for the upcoming year.

5. Implementation

The new COLA takes effect with December benefits, payable in January of the following year.

Note: If the CPI-W doesn’t increase, no COLA is applied that year. This ensures that Social Security and Supplemental Security Income (SSI) benefits adjust to reflect economic changes.

Factors influencing COLA

Cost of living adjustment is influenced by various factors, including inflation measures, adjustment frequency, regional and personal variations, and tax implications.

1. Inflation Measures

Various indices, such as the Consumer Price Index (CPI) and Personal Consumption Expenditures (PCE) index, are used to measure inflation. The choice of the index can affect COLA calculations.

2. Adjustment Frequency

Cost of living adjustment is applied at regular intervals, such as annually, which may not always match actual changes in living costs.

3. Regional and Personal Variations

The cost of living varies across regions and individuals, but COLA is often based on national or regional averages, which may not reflect personal expenses and consumption patterns.

4. Tax Implications

COLA can affect taxable income and tax liability, depending on the type of income or benefit and applicable tax rules.

COLA Calculator

COLA is determined using the Consumer Price Index (CPI), an economic indicator that tracks the average change in prices for a variety of goods and services commonly purchased by households. The Bureau of Labor Statistics (BLS) is responsible for calculating the CPI on a monthly basis and making the data publicly available on their official website.

To understand and estimate your COLA, you must know the COLA formula and how the COLA calculation works.

COLA = (Current CPI – Previous CPI) / Previous CPI * 100

For instance, if the CPI increased from 150 to 155 in the past year, here’s how to calculate the cost of living adjustment.

COLA = (155 – 150) / 150 * 100 = 3.33%

This percentage indicates the increase in prices, and as a result, wages or benefits would be adjusted by this percentage to offset the impact of inflation on purchasing power.

Let’s consider two retirees, Mark and Lisa, who receive Social Security benefits.

Mark’s current monthly benefit is $1,800, and Lisa’s is $2,200. Using the COLA percentage calculated earlier (3.33%), their new monthly benefits would be:

Mark’s new benefit = $1,800 * (1 + 0.0333) = $1,859.94 Lisa’s new benefit = $2,200 * (1 + 0.0333) = $2,273.26

What Is the COLA for 2024?

SSA has announced a 3.2% Cost-of-Living Adjustment for 2024. This increase is based on the rise in the CPI-W from the third quarter of 2022 through the third quarter of 2023.

Let’s understand the key changes in the cost of living adjustment in 2024 in detail.

- Maximum Taxable Earnings for Social Security Portion (OASDI only): $168,600

- Retirement Earnings Test Exempt Amounts:

- Under full retirement age: $22,320/yr. ($1,860/mo.)

- The year an individual reaches full retirement age: $59,520/yr. ($4,960/mo.)

- Maximum Social Security Benefit for a Worker Retiring at Full Retirement Age: $3,822/mo.

- SSI Federal Payment Standard:

- Individual: $943/mo.

- Couple: $1,415/mo.

For a more detailed breakdown of the changes in the cost of living adjustment in 2024, please refer to the PDF.

COLA 2023 VS COLA 2024

As discussed above, COLA ensures that Social Security benefits keep pace with inflation. Let’s compare the cost of living adjustment 2023 and the cost of living adjustment 2024 to understand how these adjustments impact beneficiaries.

COLA 2023:

In 2023, Social Security beneficiaries received a substantial 8.7% COLA, the largest increase in over 40 years. This significant adjustment was a result of high inflation rates in 2022. The 8.7% COLA translated to an average increase of about $146 per month for retirees.

COLA 2024:

For 2024, the Social Security Administration has announced a more moderate COLA of 3.2%. This adjustment is based on the change in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) from the third quarter of 2022 to the third quarter of 2023. The 3.2% COLA will result in an average increase of approximately $59 per month for Social Security recipients.

Let’s understand how the cost of living adjustment 2023 and the cost of living adjustment 2024 impact different aspects of Social Security in this table.

| Metric | 2023 | 2024 |

| COLA | 8.7% | 3.2% |

| Average Monthly Increase | $146 | $59 |

| Maximum Taxable Earnings | $160,200 | $168,600 |

| Retirement Earnings Limit | ||

| – Under Full Retirement Age | $21,240/yr | $22,320/yr |

| – Year of Reaching Full Retirement Age | $56,520/yr | $59,520/yr |

| SSI Federal Payment – Individual | $914/mo | $943/mo |

| SSI Federal Payment – Couple | $1,371/mo | $1,415/mo |

| Average Monthly Social Security Benefits | Before 8.7% COLA | After 3.2% COLA |

| – All Retired Workers | $1,681 | $1,907 |

| – Aged Couple, Both Receiving Benefits | $2,734 | $3,033 |

| – Widowed Mother and Two Children | $3,238 | $3,653 |

| – Aged Widow(er) Alone | $1,567 | $1,773 |

| – Disabled Worker, Spouse, and One or More Children | $2,407 | $2,720 |

| – All Disabled Workers | $1,362 | $1,537 |

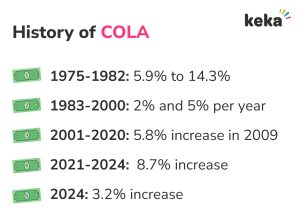

History of COLA

Cost of living adjustment was introduced in 1975 as a means to help Social Security benefits keep pace with inflation. Prior to the implementation of automatic COLAs, Congress had to approve benefit increases through legislation, which often resulted in long periods without adjustments.

Since its introduction, COLA has played a vital role in maintaining the purchasing power of Social Security benefits. However, the adjustment has varied significantly over the years, reflecting changes in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W).

Here’s how COLA changed over time.

- 1975-1982: COLAs were generally high, ranging from 5.9% to 14.3%, due to high inflation rates.

- 1983-2000: COLAs moderated, typically falling between 2% and 5% per year.

- 2001-2020: COLAs fluctuated, with some years seeing no increase (2010, 2011, and 2016) and others experiencing more significant adjustments, such as the 5.8% increase in 2009.

2021-2024: Recent years have seen relatively high COLAs, with an 8.7% increase in 2023 and a 3.2% increase in 2024, driven by post-pandemic inflation.

Having said that, let’s look at the history of COLA.

| Year | COLA |

| 2024 | 3.2% |

| 2023 | 8.7% |

| 2022 | 5.9% |

| 2021 | 1.3% |

| 2020 | 1.6% |

| 2019 | 2.8% |

| 2018 | 2.0% |

| 2017 | 0.3% |

| 2016 | 0.0% |

| 2015 | 1.7% |

| 2014 | 1.5% |

| 2013 | 1.7% |

| 2012 | 3.6% |

| 2011 | 0.0% |

| 2010 | 0.0% |

| 2009 | 5.8% |

| 2008 | 2.3% |

| 2007 | 3.3% |

| 2006 | 4.1% |

| 2005 | 2.7% |

| 2004 | 2.1% |

The average cost of living adjustment over the last 20 years is 2.62%.

COLA Projection for 2025

According to The Senior Citizens League, the COLA for 2025 is projected to be around 2.66% based on the most recent CPI-W data. However, this estimate is subject to change as the actual cost of living adjustment will be determined by comparing the CPI-W in the third quarter of 2024 to the third quarter of 2023.

How Does COLA Impact a Business?

COLA can significantly impact various aspects of a business, from employee retention and financial planning to operational goals and stakeholder management. Here are 6 ways COLA impacts businesses.

1. Employee Retention

Implementing COLAs can help businesses retain top talent by ensuring salaries keep pace with inflation. This leads to a more motivated and stable workforce.

2. Financial Planning

Cost of living adjustment requires careful financial planning to balance employee compensation with the company’s fiscal health and strategic goals.

3. Operational Goals

Regular salary increases may impact a company’s ability to adapt and grow. It could also affect operational objectives and flexibility in a changing economic landscape.

4. Employee Expectations vs. Executive Decisions

Balancing employee expectations for COLAs with the need to maintain the organization’s financial well-being can lead to difficult decisions for executives.

5. Union Negotiations

COLAs are often a mandatory part of collective bargaining agreements in unionized industries. This adds complexity to compensation structures and business operations.

6. Competitive Positioning

Offering COLAs can differentiate a company from its competitors and make it more attractive to potential employees and customers who value fair compensation practices.

Wrapping Up

The Cost-of-Living Adjustments (COLA) play a vital role in ensuring that Social Security benefits keep up with inflation. It allows beneficiaries to maintain their purchasing power over time. Without these annual adjustments, the value of benefits would diminish and make it harder for millions of Americans to afford essential goods and services.

For 2024, the Social Security Administration has announced a COLA of 3.2%, which will provide a measure of relief to beneficiaries facing rising costs. Although this adjustment is lower than the exceptional 8.7% COLA in 2023, it remains higher than the 2.6% average over the past 20 years.

FAQ:

1. What is the full form of COLA?

COLA stands for Cost-of-Living Adjustment.

2. What is COLA?

COLA is an annual adjustment to Social Security benefits and some other forms of income to help maintain purchasing power in the face of rising prices due to inflation.

3. Can COLAs differ between urban and rural areas?

Yes, COLAs can differ between urban and rural areas as the cost of living varies depending on factors such as housing, transportation, and access to goods and services.

4. Are COLAs mandated by federal or state regulations?

COLAs for Social Security benefits are mandated by federal law. Some states and local governments may have their own COLA policies for pensions and other benefits.

5. How do COLAs impact wage negotiations and employee compensation in the US?

COLAs can influence wage negotiations as employees seek to maintain their purchasing power. Employers must balance the need for competitive compensation with the financial impact of regular salary increases.

6. How do COLAs affect employee relocation and mobility within the US?

COLAs can impact employee relocation decisions as the cost of living varies significantly across different regions. Employees may seek higher salaries or COLAs when moving to areas with a higher cost of living.